If rankings reflect sentiment, capital flows reveal conviction.

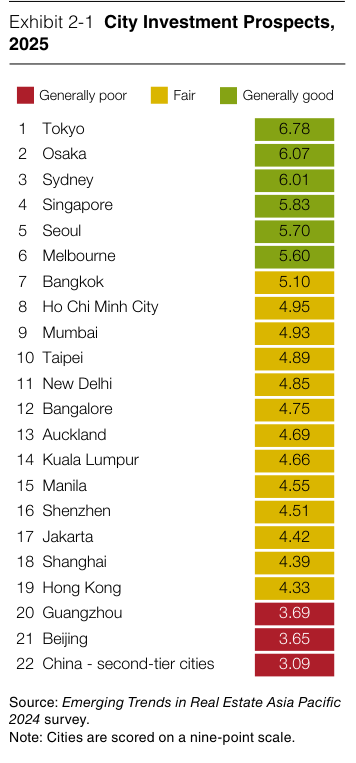

The 2025 edition of Emerging Trends in Real Estate Asia Pacific highlights that Japan remains the most preferred property investment destination in the region. In the report’s 2025 Investment Prospects ranking, Tokyo is placed first, followed closely by Osaka.

This is more than a perception indicator. It reflects where institutional investors see relative safety and long-term resilience.

The report also notes that Japanese real estate has increasingly become a “natural alternative” for capital that might previously have been directed to other Asia countries. Rather than a short-term cyclical shift, this suggests a broader structural reallocation of capital within Asia.

Tokyo: The Region’s Core Investment Market

Tokyo continues to function as the region’s primary gateway for institutional real estate investment.

Global funds are attracted by the city’s market depth, transparent regulatory environment and large pool of institutional-grade assets. These factors support liquidity and allow investors to deploy capital at scale.

For many international investors, Tokyo serves as the pricing benchmark for Japan’s real estate market, anchoring valuations across sectors such as office, residential and logistics.

The city’s mature financial ecosystem, deep tenant base and consistent transaction activity provide the level of transparency and predictability that institutional investors seek when allocating long-term capital. As a result, Tokyo often forms the core allocation within Japan-focused real estate portfolios.

Osaka: Yield and Growth Within the Capital Zone

While Tokyo anchors the market, Osaka has increasingly drawn attention as a complementary investment destination.

The report notes that large numbers of foreign buyers are actively competing for property deals in Japan. Such intensified bidding activity usually reflects confidence in three fundamentals: enforceable property rights, stable income streams and transparent exit mechanisms.

Osaka sits directly within this capital concentration zone. Compared with Tokyo, Osaka typically offers a yield premium while maintaining strong rental demand supported by its large urban population and diversified economy.

Ongoing urban regeneration initiatives and major infrastructure projects are also reinforcing long-term growth expectations.

Rising Demand for Residential Assets

In the sector overview, the report also identifies “living assets” — particularly multifamily housing — as one of the most sought-after asset classes in Asia Pacific. Japan, by a wide margin, represents the region’s largest multifamily market.

👉🏽READ MORE: Weak Yen, Strong Inflows: Capital’s Impact on Japan’s Core Assets

👉🏽READ MORE: MUFG to launch $680 million Japan real estate fund

For cities like Osaka, this trend strengthens the investment case. As global capital increasingly favours stabilised residential portfolios and core income-producing assets, Osaka offers a combination of yield advantage, strong tenant demand and institutional liquidity.

Some fund managers caution that tight pricing has made transactions harder to secure. Yet this difficulty itself reflects the intensity of capital competition.

Capital does not compete in shrinking markets. It competes where it expects durability. Japan’s market today exemplifies this dynamic.

{kind=link}

{kind=link}

{kind=link}